Singapore, Apr 1: The emergence of Guinea’s Simandou as a large-scale, high-grade iron ore supplier signifies a significant change in the global seaborne iron ore market. According to Wood Mackenzie, this project is set to be the primary catalyst for long-term supply growth.

Wood Mackenzie expects Simandou to export around 16 million tonnes in 2026, with volumes rising progressively thereafter. However, ramp-up is likely to be uneven, with infrastructure bottlenecks and logistical complexities driving a phased and non-linear increase in output.

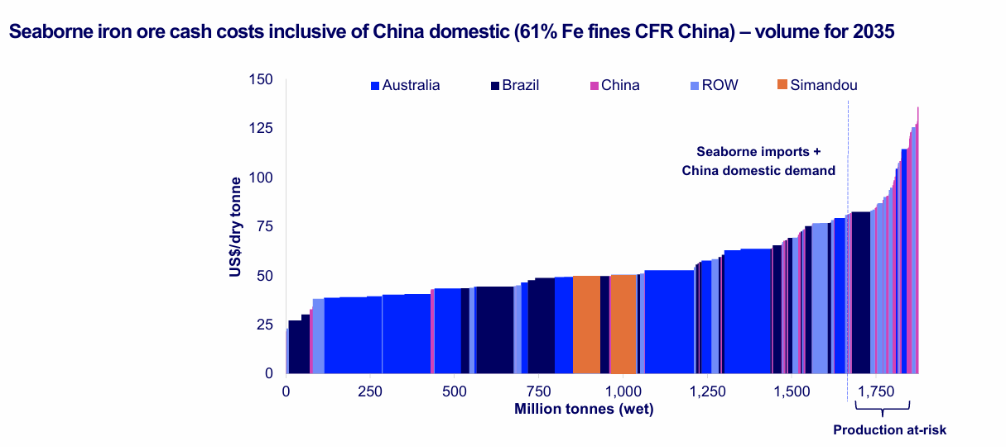

After more than two decades of delays, the project has entered execution following Guinea’s political reset in September 2021, which resolved a long-standing development deadlock. Development has progressed steadily, with early exports now in focus and downstream market impacts beginning to emerge.

Rather than simply adding volume, Simandou is expected to displace higher-cost supply, tightening the competitive landscape and reinforcing a sharper cost and quality hierarchy across the seaborne market. “Simandou will become the single biggest driver of seaborne supply growth over the coming decade,” said David Cachot, research director for iron ore at Wood Mackenzie. “But its impact goes beyond volume. These tonnes will increasingly displace higher-cost supply, reshape the cost curve and reinforce the market’s shift toward higher-quality material.”“The ramp-up will not be linear, and that uncertainty will be a key factor shaping market sentiment in the near term,” Cachot added.

Australia: blending advantages under pressure

For Australian producers, near-term impacts remain manageable, Wood Mackenzie remarked. The Pilbara continues to benefit from blending optionality, with lower-grade ores clearing the market efficiently when combined with higher-quality material. However, this advantage is expected to erode over time. As Simandou ramps up and demand preferences shift toward higher-quality feedstocks, competitive pressure is likely to emerge first in lower-grade supply.

“This does not imply an abrupt displacement of Pilbara volumes,” Cachot noted. “Rather, it highlights where pressure will emerge first, as marginal tonnes become increasingly vulnerable in a more quality-sensitive market.”

Brazil: direct premium competition

The competitive interaction with Brazil is more direct. Brazilian producers, particularly Vale, compete head-to-head with Simandou on quality, prompting a shift toward greater portfolio flexibility.

Rather than defending every premium tonne, producers are increasingly optimising product mix, including blending strategies and selective use of third-party material. While high-grade Brazilian supply remains well positioned over the longer term, increased competition in premium segments may place pressure on realised premia, Wood Mackenzie noted.

Africa: expanding supply base

Simandou sits within a broader wave of African supply development, alongside emerging projects in Gabon, Congo, and Algeria. Together, these developments point to a more geographically diversified and increasingly Africa-centric supply landscape.

This expansion reinforces Simandou’s role as a catalyst for structural change, accelerating shifts in global trade flows and intensifying competition for incumbent exporters.

Demand shifts reinforce quality premiums

Simandou’s emergence coincides with broader structural shifts in steelmaking, including industry consolidation, decarbonisation pathways, and the growth of Direct Reduced Iron (DRI) production.

These trends reinforce demand for high-grade, low-impurity feedstocks, supporting structurally higher premia for suitable products. As steelmakers prioritise efficiency and emissions reduction, raw material quality is becoming increasingly central to competitiveness.

“The strategic importance of high-grade iron ore in enabling lower-emissions steelmaking is becoming increasingly clear,” Cachot concluded. “DRI and other emerging technologies remain highly sensitive to feedstock quality, reinforcing long-term demand for premium products.”